The global FX market rarely sleeps. Even when the U.S. data calendar fades into silence, the tape hums with a nervous, almost sentient rhythm — part heartbeat, part Morse code — transmitting whispers of politics, policy, and credit from desks half a world apart. This week, that hum has narrowed to two frequencies: Paris and Tokyo. Both are signaling that the world’s glide path remains intact, but the engines beneath are quietly shifting torque — the kind of subtle power transfer that traders feel before they see.

In France, Emmanuel Macron managed to do what few expected — he handed the euro a reprieve without firing a single fiscal shot. His hint that a new prime minister could be named before the weekend was less a political announcement and more a message to the markets: “We’re not in crisis.” The effect was immediate. The OAT–Bund spread, which had ballooned toward the high-80s and threatened to reignite that old French risk premium, snapped back into the low-80s like a pressure valve releasing steam. Betting markets slashed the odds of a snap election in half. France, in trader terms, just walked itself back from a volatility cliff — and the euro, clinging to the 1.16 handle that felt like the edge of a ravine days ago, exhaled in relief.

But this isn’t a rally built on economic foundation. It’s a political ceasefire dressed as market confidence — a temporary truce between fear and apathy. In FX, perception is oxygen, and even the faintest hint of stability can turn short sellers into sideline spectators or reluctant buyers. The single currency, still boxed between 1.1580 and 1.1620, trades less like a conviction call and more like a sentiment barometer — a mood trapped in a narrow range, bouncing between restraint and fatigue. The real questions remain unanswered: will Europe’s disinflation story deepen, and can the ECB’s “good place” on rates really hold without a pivot? For now, the market seems content to dribble along, waiting for the next big shove.

Across the Pacific, Tokyo is writing a very different script. The yen has once again been cast as global finance’s reluctant hero and willing victim — the cheap fuel for everyone else’s risk appetite. USD/JPY blasted through 152 like it was tissue paper, not because traders suddenly believe in the dollar, but because they’ve rediscovered the yen’s addictive cheapness. The irony is delicious: the same currency that torched portfolios in the last carry unwind is back in vogue, fueling bets from São Paulo to Seoul. A move to 155 no longer sounds outrageous — it’s whispered with the casual inevitability of traders who’ve seen this movie before.

In Japan, politics has turned from drama to quiet choreography. Newly installed LDP leader Sanae Takaichi is still assembling her coalition, but the takeaway for markets is continuity, not confrontation. As long as that script holds, so does the BoJ’s caution. With Japanese yields anchored near zero, the yen remains a borrower’s delight. What could upend this easy-money waltz? Three things: a sharp dollar data dovish correction, a BoJ surprise hike, or a global de-risking panic. All plausible, none visible. Until one materializes, traders will keep borrowing yen to dance another round. Even the skeptics have a hard time refusing — in this game, fear of missing out is the most persuasive macro signal of all.

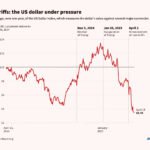

Meanwhile, the dollar’s swagger has turned into something closer to a measured shuffle. The hawkish notes buried in the latest FOMC minutes barely ruffled Treasuries, proof that the market has learned to separate Fed theatre from Fed intent. Policymakers talk tough, but traders have stopped applauding. The central bank’s confidence in the growth outlook is still intact, but with the government shutdown leaving key labor data dark, it’s navigating half-blind. The DXY, comfortably caged between 98.50 and 99.20, mirrors that mood — a kind of suspended animation where neither fear nor euphoria has the upper hand. And when momentum loses its grip, capital doesn’t sleep; it migrates. Right now, it’s migrating toward the carry complex, where yield still pays and volatility still snoozes.

And that’s the illusion — the still pond hiding an undercurrent. The euro drifts on borrowed calm, the yen powers speculative excess, and the dollar feels like a bystander. The FX market’s current phase is defined by positioning, not conviction — a world where traders make money not by believing, but by front-running those who still do.

The surface looks serene, but anyone who has traded long enough knows the sound beneath: that faint hum of shifting power, the distant echo of risk realignment. The music hasn’t stopped. It’s just changed key — and the next bar, when it comes, won’t be gentle.

{kind=link}