As global stock markets plunged on Monday, financial analysts pointed to an esoteric trade involving the Japanese yen as a key factor for the decline. Markets have since rebounded but, with volatility surging and investors feeling skittish, there are fears that the unwinding of the yen-based “carry trade”—which describes profiting off interest rate spreads across different currencies—could drive further losses.

The popularity of the Japanese carry trade is easy to understand. While central banks such as the Federal Reserve increased interest rates in the face of inflation, the Bank of Japan kept its interest rate near zero—or even lower—to incentivize economic growth. As a result, investors such as hedge funds would borrow the yen on the cheap to move into assets with higher growth potential, such as U.S. Treasuries, stocks, and other currencies. “It’s one of these trades that was a no-brainer for a lot of people,” said Chester Ntonifor, a foreign exchange strategist for BCA Research, in an interview with Fortune.

That all changed in late July when the Bank of Japan increased its interest rate to 0.25% amid concern about the yen falling against the U.S. dollar. Suddenly, with the yen rising in strength, many investors were forced to exit their positions, including through potential margin calls and liquidations. “It’s a classic case of up the staircase and down the elevator shaft,” Scotiabank chief currency strategist Shaun Osborne told Fortune. “When everyone tries to get out the door at the same time, it becomes very crowded and gets ugly.”

Market impact

While the popularity of the carry trade among institutional investors is indisputable, its exact magnitude—and its impact on Monday’s calamitous stock market decline—is still an open question.

Both Osborne and Ntonifor told Fortune it would be difficult to quantify how much money had flowed into the carry trade, but Osborne pointed to a key metric that demonstrated how quickly investors were fleeing. According to his estimations, short positions in the yen—meaning options contracts that borrowed the yen, betting that it would stay level or decrease in value—peaked at around $31 billion in late June. New data through last Tuesday showed that the figure halved to around $15 billion, indicating that traders were closing their positions and exiting the trade.

The S&P 500 fell 3% on Monday—its biggest one-day drop in nearly two years. Some financial experts pointed to the unwinding of the carry trade, with investors forced to exit their positions, which in turn would push down prices, to return yens that they had borrowed. Other factors, including a disappointing jobs report, also contributed to the decline. Still, Osborne described the carry trade as a “self-feeding mechanism,” where more money will continue to flow out until market sentiment improves. “The risk is certainly tilted toward more equity market weakness in the near term,” he said.

And while Japan’s stock market index, the Nikkei, suffered its worst daily loss on Monday since 1987, a staggering rebound on Tuesday indicates that the Bank of Japan’s strategy could be working, with yens rushing back into the country. “You have inflows into Japanese assets, which will help Japan relative to the rest of the world,” Ntonifor told Fortune, arguing that investors have been undervaluing the yen.

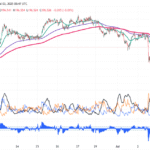

The chart below shows the precipitous decline—and sudden rebound—of the Nikkei, matched by a drop in U.S. equity prices:

What comes next?

The current drama over the yen may be far from over. Arindam Sandilya, JPMorgan’s co-head of global FX Strategy, told Bloomberg TV on Tuesday that the carry trade unwind is only 50%–60% complete. Ntonifor estimated that the process will take another two to three months, although he added that the Bank of Japan is unlikely to institute further rate hikes.

As traders exit their positions, the yen could continue to gain in value, forcing other investors out and exacerbating the trend. Other wild cards could also come into play, including the U.S. election. Former president Donald Trump said in July that one of his second-term priorities is a weaker dollar relative to the yen, which some analysts say contributed to the Japanese currency’s rally.

Although the carry trade has long been one of the most consistent strategies for investors, its abrupt lack of viability will continue to ripple across global markets. “When these situations correct, they do correct usually in a fairly spectacular manner,” said Osborne. “That points to volatility certainly persisting for a little bit longer here.”

{kind=link}